For many seniors on fixed incomes, the cost of daily medications can be just as overwhelming as medical bills. If you’re taking one or more generic drugs - like lisinopril for blood pressure, metformin for diabetes, or atorvastatin for cholesterol - Medicare Extra Help can cut your out-of-pocket costs to as little as $1.60 per prescription. This isn’t a discount or a coupon. It’s a federal subsidy built into Medicare Part D that removes nearly all financial barriers to essential medications.

What Medicare Extra Help Actually Covers

Medicare Extra Help, officially called the Part D Low-Income Subsidy (LIS), doesn’t just lower your drug costs. It wipes out your entire Part D premium and deductible. In 2025, if you qualify, you pay nothing for your monthly Part D plan fee - even if your plan normally costs $40 or more. You also don’t pay the $595 deductible that most Part D enrollees must meet before coverage starts. That alone saves hundreds of dollars each year.

For generic prescriptions, your copay is capped at $4.90 per fill. If you’re enrolled in both Medicare and Medicaid with income below 100% of the Federal Poverty Level, your copay drops further to just $1.60. That’s less than the cost of a cup of coffee. Compare that to someone without Extra Help: after paying the $595 deductible, they’d pay 25% of the drug’s cost. A $50 generic could cost $12.50 per prescription. Multiply that by 12 pills a month - $150 a month, or $1,800 a year. With Extra Help? $705.60 annually. And that’s before the premium and deductible savings.

Who Qualifies for Extra Help in 2025

Eligibility is based on two strict numbers: income and resources. For 2025, an individual can’t earn more than $23,475 per year. For a married couple living together, the limit is $31,725. Income includes Social Security, pensions, wages, and veterans benefits. But it doesn’t include housing assistance, food stamps, or Medicaid-covered medical care.

Resources are trickier. These are things you own that can be turned into cash. The limit is $17,600 for an individual, $35,130 for a couple. This includes bank accounts, stocks, bonds, mutual funds, and IRAs. But your primary home, one car, household goods, and personal items don’t count. There’s also a $1,500 allowance for burial expenses that’s excluded from the resource total.

Many people think they’re too rich to qualify - until they look at their actual finances. A $20,000 savings account might disqualify you, even if you only get $18,000 a year in Social Security. The rules don’t care about your lifestyle. They care about the numbers on paper.

How Extra Help Compares to Standard Part D

Without Extra Help, you’re stuck with the standard Part D structure: pay the deductible, then pay 25% coinsurance until you hit the coverage gap. Even after that, you pay 25% of the drug cost until you reach catastrophic coverage. For someone on multiple generics, that adds up fast.

Extra Help changes the game. No deductible. No coinsurance. No coverage gap. Just a flat $4.90 (or $1.60) for every generic. It’s not just cheaper - it’s predictable. You know exactly what you’ll pay each month. No surprises. No bills. No confusion about how much you owe after each refill.

Studies show this predictability matters. The Medicare Payment Advisory Commission found that Extra Help recipients are 23 percentage points more likely to take their medications as prescribed. For someone with heart disease or diabetes, that’s the difference between staying out of the hospital and ending up in the ER.

How to Apply - And Why Most People Miss Out

You don’t have to be told about Extra Help. The system doesn’t automatically enroll you. You must apply. And here’s the problem: 37% of eligible people never do. Why? The application is confusing. The forms are long. People think they need a lawyer or a financial advisor. They don’t.

You can apply online at SSA.gov. Or call 1-800-772-1213. Or walk into your local Social Security office. If you’re already getting Medicaid, Supplemental Security Income (SSI), or a Medicare Savings Program, you’re automatically enrolled. But if you’re not? You need to fill out the form.

State Health Insurance Assistance Programs (SHIPs) offer free, one-on-one help. They’ve helped over 70% of applicants complete the process correctly. You don’t need to know the rules. You just need to show up with your income documents - Social Security award letter, bank statements, tax returns, pension statements. They’ll do the rest.

What Happens After You Get Approved

Once approved, your Part D plan will be updated automatically. You’ll start seeing $4.90 copays at the pharmacy. You’ll get a new Medicare & You handbook in the mail. You’ll also get a letter every August asking you to recertify. This is critical. If you don’t return it within 30 days, your benefits stop on January 1 - no warning, no grace period.

Also, you can switch your Part D plan once a month. That’s a special enrollment period just for Extra Help recipients. If your current plan stops covering a drug you need, you can change plans right away. You don’t have to wait for open enrollment.

The Real-Life Impact - And the Hard Cuts

One Reddit user, a retired pharmacist, said: "I’ve seen patients skip their blood pressure meds because they cost $30 a month. The moment they got Extra Help, their copay dropped to $4.90. Their numbers stabilized. They stopped going to urgent care. It changed their life."

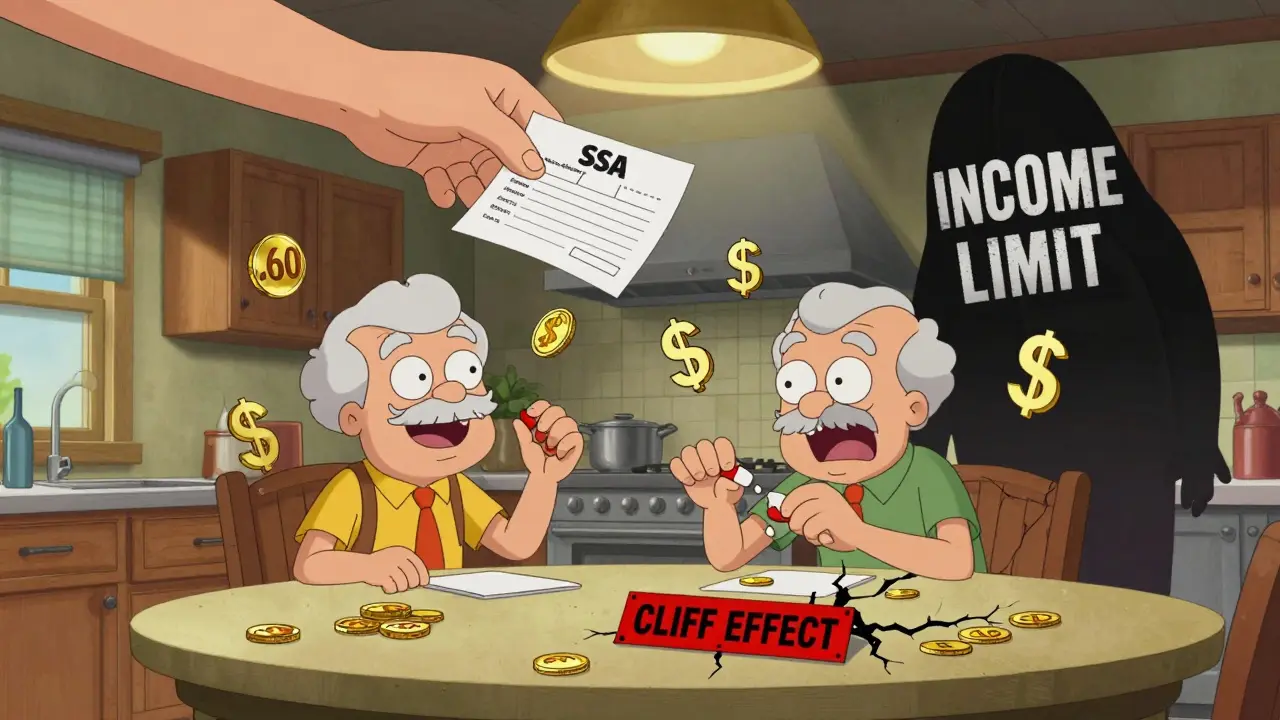

But there’s another side. Another user wrote: "I made $500 more than the income limit because my Social Security went up. I lost Extra Help overnight. My $200-a-month generic drugs now cost me $1,200 a year in premiums plus $748 in copays. I can’t afford it. I’m cutting pills in half."

This is the "cliff effect." The program doesn’t phase out benefits gradually. One dollar over the limit - and you lose everything. That’s why experts call it a broken system. AARP and the Kaiser Family Foundation have pushed for expansion, suggesting eligibility go up to 175% of the Federal Poverty Level. That would cover over a million more people.

What’s Next? Changes Coming

The Inflation Reduction Act already capped insulin at $35 a month for all Medicare beneficiaries - including those with Extra Help. That’s a bonus, not a replacement. Extra Help still saves more on other generics.

There’s talk of expanding eligibility further. If Congress passes the Biden administration’s 2025 proposal, the income limit could rise to $28,500 for individuals. That would mean more people qualify. But until then, the rules stay strict.

The program is funded with $52.7 billion in 2025. It’s not going away. But it’s not growing either - unless pressure from seniors and advocates forces change.

What You Should Do Now

If you’re on Medicare and take any generic drugs - even one - check your eligibility. Don’t assume you make too much. Don’t wait for a letter. Don’t think it’s too complicated.

- Go to SSA.gov and use the Extra Help eligibility tool.

- Call 1-800-772-1213 and ask for the Extra Help application.

- Contact your local SHIP office - they’ll help you for free.

- Gather your income documents: Social Security award letter, bank statements, tax return.

- Apply before August 31 to avoid losing benefits next year.

There’s no downside to applying. If you don’t qualify, you lose nothing. If you do - you could save thousands. For many, it’s the difference between taking your medicine and skipping it.

Do I need to reapply for Extra Help every year?

No, you don’t need to reapply from scratch. But you must complete an annual review each August. You’ll receive a form in the mail asking you to confirm your income and resources. If you don’t return it within 30 days, your Extra Help benefits will stop on January 1. Many people lose coverage simply because they ignore this form.

Can I still get Extra Help if I have savings in the bank?

Yes - but only if your total countable resources are below $17,600 (individual) or $35,130 (couple). Your primary home, one car, and personal belongings don’t count. But cash, stocks, bonds, mutual funds, and IRAs do. Even $18,000 in savings could disqualify you. It’s not about how much you spend - it’s about what you own.

Does Extra Help cover brand-name drugs too?

Yes, but at a higher cost. For brand-name drugs, the maximum copay is $12.15 in 2025. Most people on Extra Help use generics because they’re cheaper and just as effective. If you need a brand-name drug because no generic exists, Extra Help still helps - but you’ll pay more than the $4.90 you’d pay for a generic.

Can I switch my Part D plan if I get Extra Help?

Yes - and you can do it every month. Most Medicare beneficiaries can only change plans during the annual open enrollment. But Extra Help recipients get a Special Enrollment Period. If your drug isn’t covered, or your pharmacy network changes, you can switch to a better plan at any time. Changes take effect the first of the next month.

What if I make too much money one year but need help the next?

You can reapply. If your income drops - because of job loss, reduced hours, or a change in benefits - you can submit a new application. Extra Help is reviewed each year, so if your financial situation changes, you may qualify again. Don’t assume you’re permanently ineligible. The rules are based on your current income, not past earnings.

Comments

Susan Purney Mark

March 7, 2026 AT 08:39 AMI just applied for Extra Help last month and got approved! My metformin used to cost me $42 a month. Now it’s $1.60. I cried at the pharmacy. 🥹 Seriously, if you’re even *thinking* about it - just apply. No downside. I didn’t think I qualified because I have a little in savings, but they only count *countable* resources. My car and house didn’t count. 🙌

Patrick Jackson

March 9, 2026 AT 01:00 AMThis program is one of those rare things in America that actually works the way it’s supposed to. I mean, think about it - $1.60 for life-saving meds? That’s not charity. That’s basic human decency. And yet we treat it like some kind of welfare lottery. People are dying because they can’t afford to take their pills. This isn’t about politics. It’s about whether we believe people deserve to live. 🤔

Pranay Roy

March 10, 2026 AT 12:38 PMYou all are being manipulated. Extra Help is a trap. The government gives you $1.60 copays so you don’t revolt. But then they raise your premiums next year and cut your Social Security. They want you dependent. I checked my bank records - they track every pill you take. It’s all part of the surveillance state. And don’t get me started on how they use your pharmacy data to sell you ads. 🕵️♂️

Andrew Poulin

March 10, 2026 AT 22:23 PMApply now. Don’t wait. August is the deadline. If you miss it you lose everything. No warning. No grace. Just gone. And if you think you make too much money you’re wrong. My sister made $24k and got denied. She had $16k in savings. That’s it. One thousand dollars over and she lost it all. Just apply. It takes 15 minutes.

Sean Callahan

March 11, 2026 AT 01:09 AMI lost Extra Help last year because i forgot to send the form. I was so stressed i started cutting my pills in half. My bp went crazy. I had to go to the er. Now i have a note on my fridge that says "SEND FORM AUGUST". I still cry when i see it. I’m not even mad. I’m just... tired. 😔

phyllis bourassa

March 11, 2026 AT 05:04 AMI hate to say it but this whole system is a joke. People who are barely over the limit get crushed. My neighbor made $23,500 - $25 over - and lost her coverage. She’s now taking half her insulin. Meanwhile, some guy with $200k in crypto and a vacation home gets it because he’s married to someone on SSI. The rules are broken. This isn’t help. It’s a cruel lottery.

Ferdinand Aton

March 11, 2026 AT 19:07 PMWait - so you’re telling me I can switch my Part D plan every month if I have Extra Help? That’s wild. I’ve been stuck with the same plan for 4 years because I thought I had to wait. I just checked my drug list - my pharmacy doesn’t even carry my med anymore. I’m switching tomorrow. Game changer.

William Minks

March 13, 2026 AT 06:58 AMComing from India, I’m blown away. Here, we have no such program. My uncle in Delhi pays $80 a month for his blood pressure med. He skips doses. I told him about Extra Help and he cried. We’re lucky. This isn’t perfect, but it’s something. I hope more countries adopt this. 🇮🇳🇺🇸

Jeff Mirisola

March 14, 2026 AT 21:31 PMI’ve been a case manager for seniors for 12 years. I’ve seen people skip meals to afford meds. I’ve seen people sell their jewelry. Extra Help doesn’t just save money - it saves dignity. One woman told me she finally started going to church again because she didn’t have to beg for help. That’s the real win. Keep pushing. Keep applying. Don’t let them tell you you’re not worthy.

Joey Pearson

March 15, 2026 AT 21:37 PMJust applied. Took 12 minutes. Got approved in 3 days. My copay dropped from $38 to $1.60. I’m buying myself a new pair of shoes today. 🥳

Roland Silber

March 17, 2026 AT 15:00 PMOne thing nobody talks about: the recertification form. You get it in August. If you ignore it, you lose everything on Jan 1. No warning. No email. No letter. Just poof. I had a client who missed it because she was in the hospital. She didn’t even know she lost coverage until she got a $90 bill. Call your SHIP office. They’ll mail you a reminder. Seriously - don’t wait.